Are you confused about what your insurance covers for a new roof?

Are you worried about paying for code-mandated upgrades out-of-pocket?

With big home improvement projects like roof replacements, unexpected expenses like “code upgrades” can be stressful. If your roof is damaged, local building codes might require updates, which can be costly without the right insurance.

Many roofing companies, including Linta Roofing, won’t install a new roof unless it meets these code requirements. That’s why understanding code upgrade coverage is crucial. In this article, you’ll learn how to check if you have this coverage, what happens if you don’t, and how to avoid unexpected costs.

Let’s start by explaining what code upgrade coverage is.

What is Code Upgrade Coverage for a Roof?

Code upgrade coverage, also referred to as ordinance or law coverage, is an add-on to your homeowner’s insurance policy. It helps cover the cost of ensuring that your home’s repairs meet current local building codes. This type of coverage is especially important when you need to replace or repair your roof, as building codes often change over time.

For example, if your roof is damaged and needs replacement, local building codes may now require new materials or construction techniques that weren't mandated when your roof was initially installed. Without code upgrade coverage, your insurance will only cover the cost of replacing your roof to its original specifications, leaving you to pay for the upgrades required by current codes.

Which is good to know, but what’s really important is understanding whether you have code upgrade coverage or not.

How Do I Know if I Have Code Upgrade Coverage?

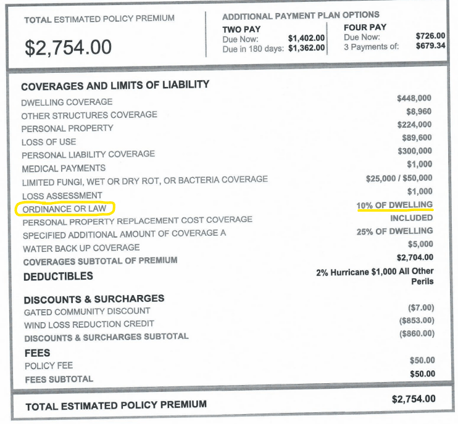

To find out if you have this coverage, the first place to look is your insurance policy’s declarations page. This is a summary of your policy and should list code upgrade coverage if it’s included. If it’s not clear or you don’t see it, contact your insurance agent to confirm. It's important to have written confirmation so you're not left with any surprises during the claims process.

Ask your agent to provide a specific excerpt from your policy that mentions code upgrade coverage. This ensures you know exactly what’s covered and avoids any misunderstanding when filing a claim. Often insurance companies use their own language, which can make this more confusing than it has to be. So, we suggest getting up to speed with insurance terms to ensure you’re understanding your policy as accurately as possible.

But, what happens if you don’t have code upgrade coverage? What can you do?

What Happens if You Don’t Have Code Upgrade Coverage for My Roof?

Let’s consider a scenario where your roof is 25 years old, and the local building code has changed to require a drip edge, which wasn't part of the original installation. If you don’t have code upgrade coverage, your insurance won’t cover the cost of adding these drip edges when your roof is replaced, meaning you’ll have to pay for it yourself. Even without coverage, contractors must comply with the latest codes, so this expense would be unavoidable. On average, most homeowners pay around $1,500+ for code upgrades when included in a full roof replacement.

This is why it’s essential to understand whether your insurance policy includes code upgrade coverage. Without it, any necessary updates required by new building codes will come directly out of your pocket. However, if you find that your roof replacement is coming at an inopportune time financially, you may be able to finance these upgrades to spread out your payment of them over time. To learn more about what’s required by South Carolina code, be sure to look at the International Residential Code requirements.

Getting code-upgrade coverage approved takes a roofer who knows the claim process; here are the Myrtle Beach roofers who handle insurance claims.

Ensuring You Have Code Upgrade Coverage for Your Roof

When insurance approves your claim, it can be very frustrating to learn that you will both pay your deductible and an unforeseen added cost to meet code requirements. Not only that, but when you’ve had to have your roof replaced unexpectedly, you may feel unprepared for this additional expense.

Thankfully insurance offers a way out, you just have to check your declarations page to see if code upgrade coverage is included in your insurance policy. And if it’s not, you can call your insurance agent and have them add it to your policy. On rare occasions, you may need to get a new policy.

As a homeowner, it’s important to understand your insurance payout as you move forward. And we at Linta Roofing are happy to provide additional assistance to help you understand the insurance process and feel informed and empowered to tackle your roofing project!

Topics:

{kind=link}