Not sure what red flags to look for in a homeowners insurance policy?

Do you feel confused by insurance lingo?

When it’s time to file an insurance claim on your roof, the last thing you want to find are surprises in your policy that require you to pay more out-of-pocket than you were expecting. This is particularly crucial for homeowners in Myrtle Beach, where we have a heavy storm season. Having helped homeowners in Myrtle Beach through the insurance claim process for nearly 40 years, we at Linta Roofing have seen homeowners pay more out-of-pocket than they expected when these 3 things are included in their policy:

When reviewing your homeowner's insurance policy, it's essential to be aware of certain expenses associated with these 3 things, particularly when it comes to roof replacements. In this article, we’ll discuss the risks you may face when these are included in your policy and better options so you can feel informed and secure with your homeowners insurance.

Homeowners Insurance Red Flag #1: ACV Policy (Actual Cash Value Policy)

If you see "ACV" or "Actual Cash Value" in your insurance policy, proceed with caution. An ACV policy means that any claims you file will be significantly depreciated. Essentially, you might receive only a fraction (often 50% or less) of the roof repair or replacement cost from your insurance company.

Why It Can be Problematic: While ACV policies often have lower premiums, they come with greater risks. Many homeowners mistakenly opt for this policy because it is less expensive, not realizing they’re sacrificing coverage. Choosing an ACV policy might protect the insurance company more than it does you, leaving you with minimal compensation when it matters most.

Instead, look for an RCV (Replacement Cost Value) policy. RCV coverage pays for repairs or replacements based on today’s costs, not a depreciated amount. The difference in premiums between ACV and RCV is usually minimal but could save you thousands if you need to file a claim.

We've worked with many homeowners who, after experiencing roof damage, found out their ACV policy would only cover about half of the replacement costs. Unfortunately, once the damage occurs, changing policy terms is no longer an option. This is a common issue homeowners face when they aren't fully aware of their policy's limitations. But this is not the only limitation to look out for, another red flag comes in the form of percentage deductibles for wind and hail damage.

Homeowners Insurance Red Flag #2: Percentage Deductibles for Wind and Hail Damage

Most insurance policies include deductibles for specific events, such as wind and hail. This is particularly important for Myrtle Beach residents, as we experience strong winds during hurricane season and plenty of hail throughout the year. A key red flag is if your policy sets deductibles as a percentage for these types of damage rather than a fixed dollar amount.

Why It Can be Problematic: Percentage deductibles can be surprisingly costly. For example, a 2% wind and hail deductible on a home insured for $400,000 means you would pay $8,000 out of pocket before insurance covers the rest. In contrast, a fixed-dollar deductible (e.g., $1,000) can save you thousands when disaster strikes.

Insurance companies often include percentage deductibles to lower premiums, making the policy seem more appealing. However, this can lead to unexpectedly high costs when filing a claim. A slightly higher annual premium for a fixed-dollar, low cost deductible can offer more predictable expenses and peace of mind.

Insurance companies often include percentage deductibles to lower premiums, making the policy seem more appealing. However, this can lead to unexpectedly high costs when filing a claim. A slightly higher annual premium for a fixed-dollar, low cost deductible can offer more predictable expenses and peace of mind.

Consider a scenario where the premium difference between a percentage deductible and a fixed-dollar deductible is $600 annually. Over 15 years, you’d pay an extra $9,000. However, if you encounter a severe storm within that period, you could save more than $10,000 on deductible costs alone.

Homeowners Insurance Red Flag #3: No Code Upgrade Coverage

Another red flag is the absence of "Code Upgrade" or "Ordinance and Law" coverage in your policy. This type of coverage is crucial for bringing your home up to current building codes when repairs are needed. Roofing contractors are required by law to ensure that their work is up to code. When you hire a reliable roofing contractor, they are likely to deny completing work on your home if you are not willing to pay for code required upgrades.

Why It Can be Problematic: Without this coverage, your insurer may only cover repairs to match your home's original structure, not the updated building codes. This means you could be responsible for the additional expenses required to meet modern standards.

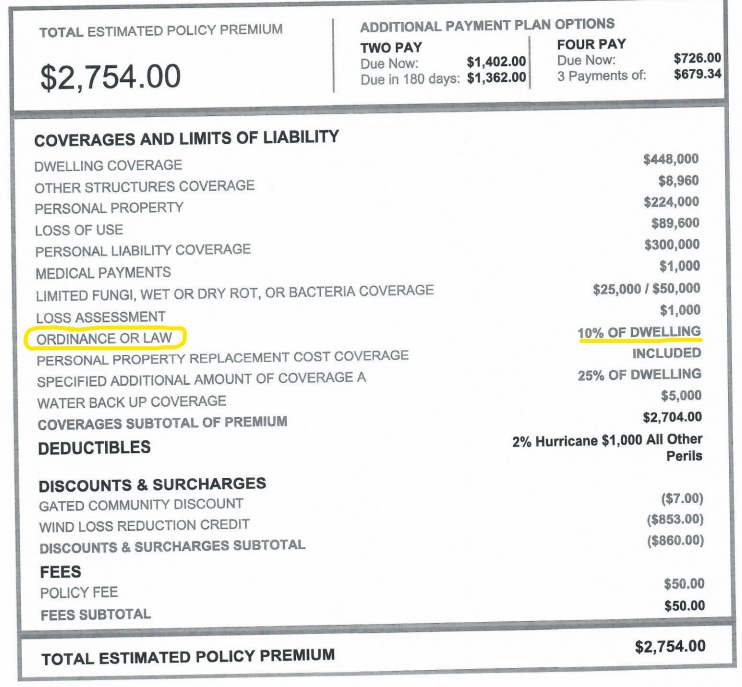

Here’s an example of what you might see on your insurance declarations page: "Ordinance and Law: 10% of Dwelling." This means that the insurer will cover up to 10% of your home's value for expenses related to code compliance. It’s important to note that all policies are different and may or may not include 10% of dwelling. The cost of adding this coverage to your policy is relatively small, often as little as $67 annually, but it can save you significantly in the long run.

Choosing the Right Homeowners Insurance in Myrtle Beach

Homeowners insurance policies can be long and confusing. Not only that, but insurance companies tend to use their own language, making it easy to miss something important.

Being vigilant about these three red flags—ACV policies, percentage deductibles for wind and hail, and the absence of code upgrade coverage—can help you avoid costly mistakes. While lower premiums might seem attractive initially, investing a bit more in comprehensive coverage could save you thousands over time. Always consult with an insurance expert or knowledgeable contractor to review your policy and ensure you have the protection you need.

If you’re thinking about making an insurance claim on your roof and you see these red flags on your insurance policy, we invite you to reach out to us for help. Repairing your home is stressful enough, we’re here to help you through the insurance claim process from start to finish!

Topics:

{kind=link}