If your roof is actively leaking, the goal tonight is to contain the water until a roofer can assess and fix the source. A temporary interior fix will not solve the problem permanently, but it will limit the damage. This guide covers what to do right now, and then explains what homeowners insurance typically covers in these situations and what it does not.

Table Of Content

- How to Stop a Roof Leak from Inside

- What Homeowners Insurance Covers for a Roof Leak

- What Insurance Typically Does Not Cover

- What a Roofing Contractor Does in the Claims Process

- Contact Linta Roofing

- Frequently Asked Questions

How to Stop a Roof Leak from Inside

Work through these steps in order.

- Put a bucket under the drip: Place a bucket, large pot, or trash can directly below the active drip. If the ceiling is visibly bulging, use a screwdriver or nail to puncture the lowest point and let the water drain in a controlled stream into your container. A bulging ceiling holds more water than it looks like from below, and if it gives way on its own, the damage spreads fast.

- Move everything out of the affected area: Get furniture, rugs, and electronics away from the wet zone before anything else gets saturated. Water damage to personal belongings is rarely covered under the same claim as structural repairs.

- Lay plastic sheeting or a tarp on the floor: Cover the floor with heavy plastic sheeting or a waterproof tarp to protect the subfloor. Water sitting on hardwood or carpet for several hours accelerates mold growth. Weigh the edges down to keep it flat.

- Find the entry point in the attic: If it is safe to access, take a flashlight into your attic and trace the water back toward the roof deck. The entry point is almost always higher than where water appears on the ceiling below. Look for wet insulation, dark staining on the rafters, or active dripping on the plywood sheathing. Place a second bucket directly below the entry point.

- Apply roofing tape or foam sealant to the entry point: From inside the attic, press waterproof roofing tape or a roofing-specific foam sealant firmly over the wet area on the sheathing. This slows or stops active intrusion through the night but does not replace a proper repair. Most DIY roof repairs create new problems if they substitute for professional work rather than bridge the gap until a roofer arrives. Standard interior caulk and general-purpose foam will not hold against moisture at this level.

- Cover the exterior if conditions allow: If the pitch is low, rain has stopped, and you can safely reach the damaged section, a heavy plastic tarp secured with sandbags or bungee cords adds another layer of protection. Never get on a wet or steep roof in the dark. If there is any doubt about safety, skip this step entirely.

- Document the damage before you clean up: Before moving buckets or drying anything out, take clear photos and video of every affected area: the ceiling, the water stains, the attic entry point, and any damaged belongings. Timestamp everything. Both your insurance adjuster and your roofing contractor will need documentation of the damage in its original state.

What Homeowners Insurance Covers for a Roof Leak

Standard homeowners insurance covers sudden and accidental damage. If a storm caused the leak, the resulting interior water damage is generally covered under your policy's dwelling protection. For a full breakdown of what storm damage typically qualifies, covered causes include:

- Wind-driven rain

- Flying debris

- Hail impact

- Falling objects such as tree branches

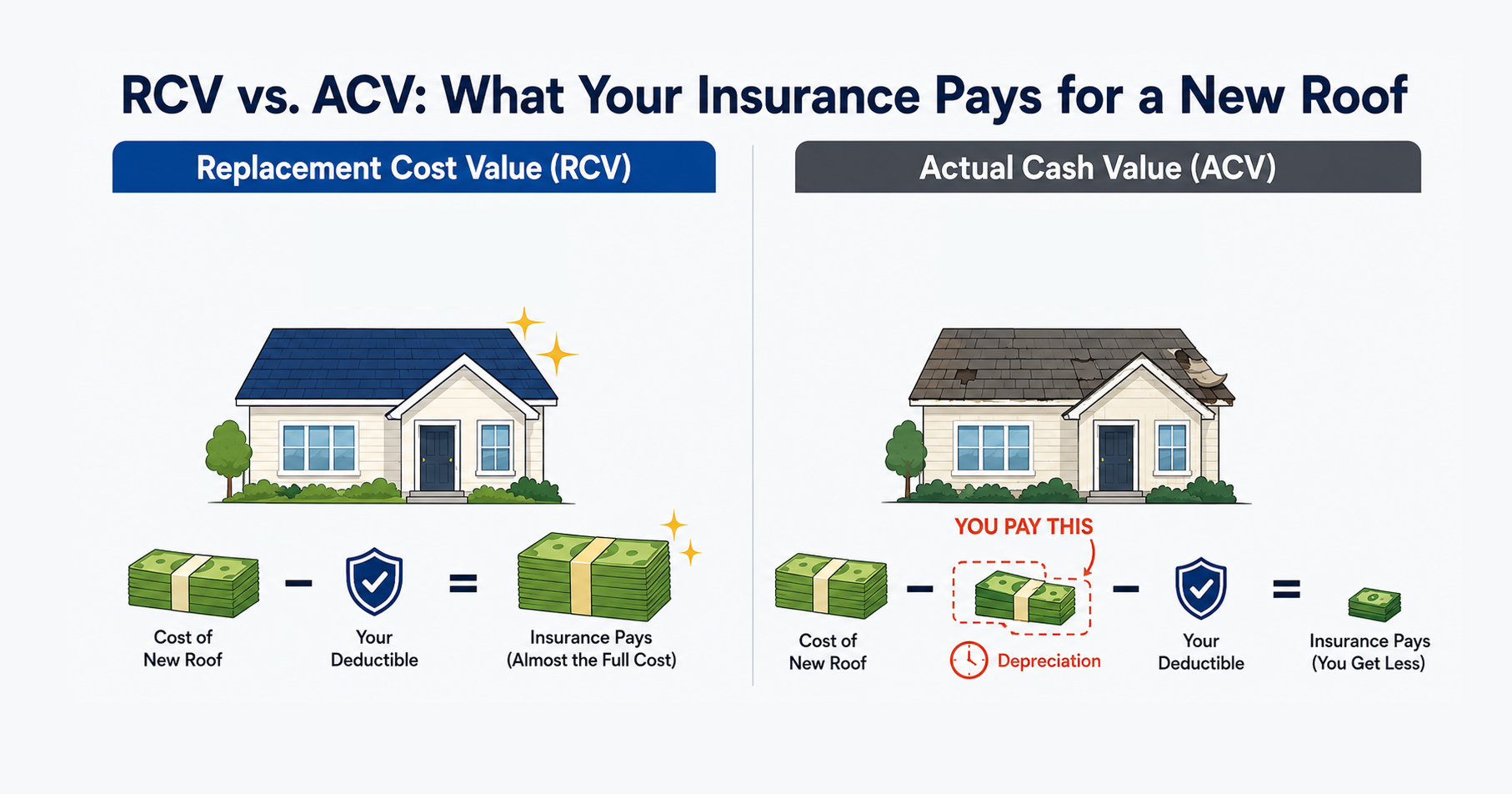

How much you receive depends on your policy type. Understanding the difference between ACV vs. RCV matters here. A replacement cost value (RCV) policy pays the full cost to replace your roof minus your deductible. An actual cash value (ACV) policy pays only the depreciated value at the time of the loss. South Carolina carriers have increasingly moved older roofs to ACV, which many homeowners do not discover until they file a claim.

Your policy may also cover emergency protective measures like a temporary tarp. Keep your receipts for anything you purchase tonight.

What Insurance Typically Does Not Cover

Insurers deny claims when damage is traced to maintenance failures rather than a storm event. There are also red flags to watch for in your policy before you file. Common denial reasons include:

- Gradual leaks from worn flashing, deteriorated sealant, or slow shingle breakdown

- Pre-existing damage that preceded the storm

- Mold remediation, unless you can show the intrusion was sudden and that you acted quickly to contain it

Your timestamped photos from tonight help establish both the cause and your response time, which matters if mold becomes an issue later.

What a Roofing Contractor Does in the Claims Process

An experienced roofing contractor does more than replace materials. On a storm damage claim, they document the cause of loss in a way that supports your case, meet with your adjuster on-site, and identify damage that a general adjuster might attribute to wear rather than the weather event.

Linta Roofing's project managers are trained to the HAAG forensic engineering standard. That is the same framework insurance adjusters use to evaluate storm damage. On the Grand Strand, where coastal storms can produce damage patterns that resemble aging, that level of documentation makes a measurable difference in how a claim is reviewed. Learn more about how our insurance claim assistance process works.

Contact Linta Roofing

Tonight's steps bought you time. A professional inspection will determine the full scope of the damage, including what is not visible from inside your attic.

Linta Roofing has served the Myrtle Beach area since 1948, holds GAF Master Elite certification, and carries an A+ BBB rating with more than 900 five-star Google reviews. We offer 24/7 emergency service for active storm damage. Contact us to schedule your inspection.

Frequently Asked Questions

Does homeowners insurance cover a roof leak after a storm?

Generally yes, for interior water damage. Whether the roof repair itself qualifies depends on the cause of the leak, your policy terms, and whether pre-existing damage is present.

How long can I wait before calling a roofer?

No more than 24 to 48 hours. A minor-looking leak can indicate broader damage that worsens with the next rain, and standing moisture accelerates mold growth.

Does my roof's age affect my claim?

Yes. On a roof 15 years or older, many South Carolina carriers apply ACV pricing, which factors in depreciation and reduces the payout. Check your policy documents for which type you carry.

Can I be reimbursed for materials I bought tonight?

In most cases, yes. Keep all receipts and include them with your claim documentation.

Topics:

{kind=link}